As shared throughout 2022, the Fed’s battle with inflation is the dominant force driving challenges in both the stock and bond markets. In addition to a challenging market, borrowers are feeling pain in the form of higher rates on mortgages, credit cards, auto loans, etc. These are the painful realities of reversing the Fed’s previous interest rate (ie. free money) and quantitative easing (QE) policies.

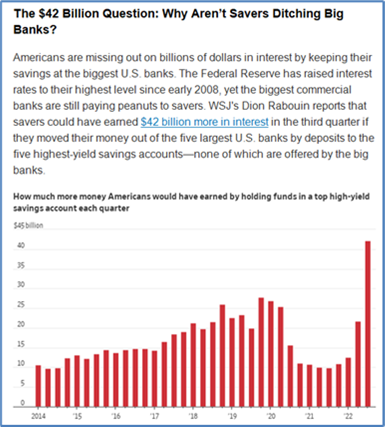

There is an attractive positive to higher interest rates however. For savers, cash is finally returning a “reasonable” rate… if you know where to look! For those seeking greater returns, opportunities exist. Reference this recent article from NerdWallet.com. Current rates vary widely, but a quick online search reveals multiple banks offering rates exceeding 3%, all while being FDIC insured (up to $250,000 per account).  One of our favorite on-line banks, Ally (www.ally.com), is currently offering a 3.30% return. Unfortunately, many banks, especially the “big banks”, are not passing these rates along to their customers. Many of the most frequently used traditional banks continue to pay next to nothing for savings – Huntington, Chase, & Fifth Third all are paying around 0.01%!

One of our favorite on-line banks, Ally (www.ally.com), is currently offering a 3.30% return. Unfortunately, many banks, especially the “big banks”, are not passing these rates along to their customers. Many of the most frequently used traditional banks continue to pay next to nothing for savings – Huntington, Chase, & Fifth Third all are paying around 0.01%!

For an even higher yield, another attractive alternative is holding “excess cash” in a Schwab position traded money market fund within your Schwab brokerage account. These funds are currently paying an attractive +4.3% yield, and for those in the highest income tax bracket, Schwab offers a Municipal Money Fund (tax-exempt) paying +3.3%. Although not FDIC insured, these money market funds are invested in the highest grade government debt and considered cash equivalents.

To be clear, a saver’s #1 priority for short-term money should always be “return of capital”, not “return on capital”. This simply means that money intended for use in the near term must be safe & 100% liquid. We continue to encourage clients to establish minimum and maximum “guard rails” for cash on-hand (remember our “Buckets of Time” concept). With that said, if you are holding growing balances of cash at the bank, in excess of a reasonable threshold, consider seeking a safe higher return. Take advantage of this new environment where interest rates continue to rise. We welcome the opportunity to discuss this idea further.

SECURE ACT 2.0 OVERVIEW

On December 29, SECURE Act 2.0 was signed into law. With strong bipartisan support for the measures, Congress included a compromise between the House SECURE 2.0 and the Senate EARN Act in the omnibus bill with 3 primary goals: Promote saving earlier for retirement while increasing some limits; Incentivize small business to offer retirement plans; Provide additional flexibility for those approaching retirement age (60+).

Key provisions include:

- The age when Required Minimum Distributions (RMDs) from retirement accounts begin increases to age 73 in 2023, and to age 75 in 2033

- Tax penalty for not taking RMDs was reduced from 50% to 25%

- The limit for catch-up contributions to 401(k)s for those aged 60 to 63 increases to $10,000 beginning in 2025, but treats those contributions as after-tax income (taxed upon deposit)

- Indexes to inflation the current $1,000 annual maximum catch-up contribution for IRAs for those aged 50 and older beginning in 2024

- Indexes to inflation the current $100,000 cap for qualified charitable distributions (QCDs)

- One-time QCD transfer of up to $50,000 through a charitable gift annuity, charitable remainder unitrust, or charitable remainder annuity trust

- Requires businesses offering new 401(k) or 403(b) plans to auto-enroll their employees in those plans (with an opt-out option) beginning at 3% of income and increasing by 1% per year to at least 10% of income, but not to exceed 15%

- Increases the tax credit for the costs of setting up a retirement plan for small businesses of up to 100 employees

Your team at Nvest will continue to study these changes in the coming months and provide more insight via future monthly commentary. We are always available to chat should you have immediate questions or thoughts.

For a comprehensive list of changes, please reference this online article.