Three-In-One: This commentary shares three shorter writings about the changing investment landscape. We hope presenting these ideas is helpful; we share our “radar screen” as we navigate these perplexing times. – Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

Price & Time

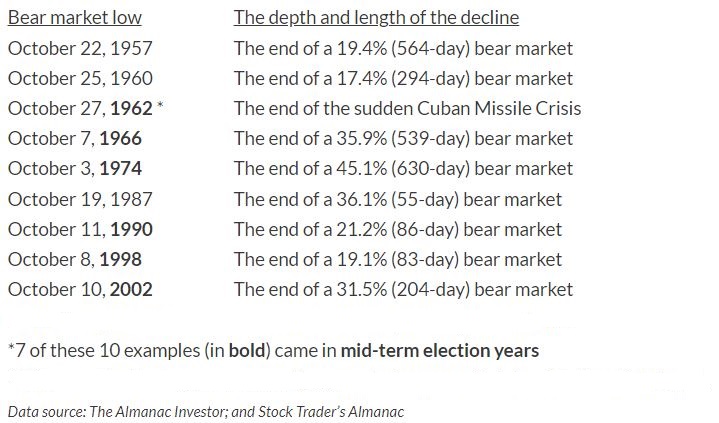

October financial market performance is often thought to be scary. That’s because some of the worst historical drawdowns occurred in October – 1929 and 1987. Interestingly a number of past bear markets also “died” in October of which several were also midterm election years.  Did you know, that September is more often a negative experience? October 2022 represents the single best performance month this year for stocks and client portfolios. It provides at least momentary respite from an otherwise trying YTD. The financial market system may be “voting” on several changing tidbits – inflation may be peak which some think should lead to a Federal Reserve pivot or pause (but that seems unlikely before 2023); company earnings are softer but better than expected; and upcoming mid-term elections may produce Washington gridlock, a condition markets generally prefer. The S&P500 advanced +8.1% during the month which generated positive client portfolio returns as well. YTD returns are still decidedly negative but improved from their quarter-end market lows.

Did you know, that September is more often a negative experience? October 2022 represents the single best performance month this year for stocks and client portfolios. It provides at least momentary respite from an otherwise trying YTD. The financial market system may be “voting” on several changing tidbits – inflation may be peak which some think should lead to a Federal Reserve pivot or pause (but that seems unlikely before 2023); company earnings are softer but better than expected; and upcoming mid-term elections may produce Washington gridlock, a condition markets generally prefer. The S&P500 advanced +8.1% during the month which generated positive client portfolio returns as well. YTD returns are still decidedly negative but improved from their quarter-end market lows.

Inflation remains a primary concern for domestic and foreign markets; Russia/Ukraine is still a troubling geopolitical, economic growth and inflationary issue. Fortunately, consumer inflation expectations are still anchored at lower levels; but current high inflation rates are not subsiding quickly, implying additional rate hikes. We feel confident the Fed is intent to bring inflation down. The question is at what cost? How long will the Fed use jumbo rate increases (+0.75%)? The Fed stated they will lower inflation and may entail some economic pain. [Investors can attest to pain in 2022; but will it affect a large population base too?] (1) Their focus is to reduce job openings without provoking job loss and arrest the wage pressure component in inflation. It’s a big challenge to aggressively raise interest rates without bringing on a recession that would raise unemployment.

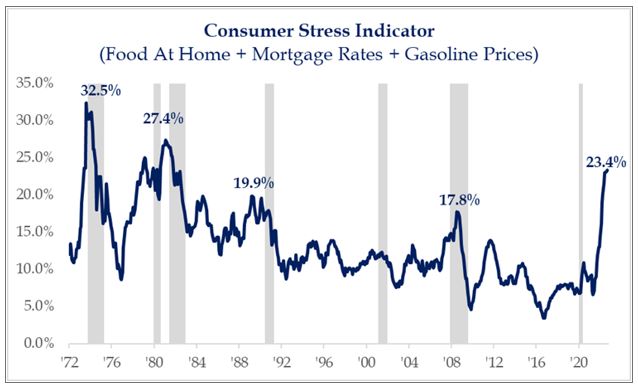

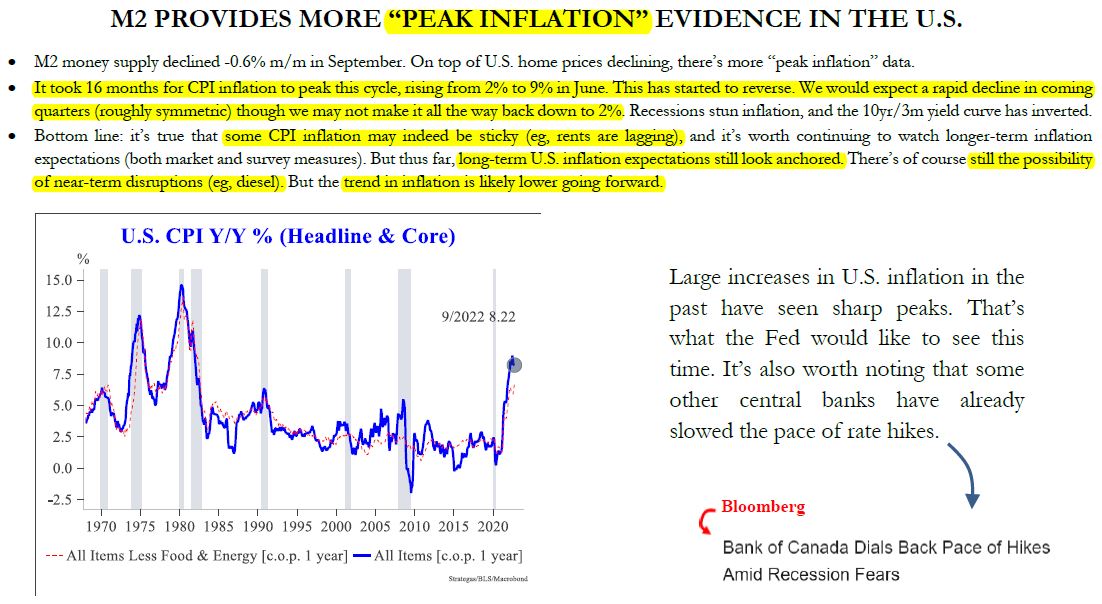

Inflation probably peaked over the summer, but Consumer Stress is still rising (Indicator is the combination of food at home + mortgage rates (now over 7%) + gasoline prices; now registers at 23.4%). Consumers are being pinched. This is unlikely to ease quickly; historically CPI changes looks like a “bell-shaped” curve. It took 16 months for CPI inflation to peak in this cycle, rising from 2% to 9% in June. This is starting to reverse. A rapid decline in coming quarters, roughly symmetric, will trend it back toward 2-3%. BUT, sticky components like rent & wages and other possible supply chain disruptions from foreign suppliers make the final rate likely higher than desired. If it took 16 months to peak, it’s likely that it will take a similar timeframe (or longer) before inflation can stabilize at lower levels.

Consumers are being pinched. This is unlikely to ease quickly; historically CPI changes looks like a “bell-shaped” curve. It took 16 months for CPI inflation to peak in this cycle, rising from 2% to 9% in June. This is starting to reverse. A rapid decline in coming quarters, roughly symmetric, will trend it back toward 2-3%. BUT, sticky components like rent & wages and other possible supply chain disruptions from foreign suppliers make the final rate likely higher than desired. If it took 16 months to peak, it’s likely that it will take a similar timeframe (or longer) before inflation can stabilize at lower levels.

Bear markets are painful to endure. In recent years, investors experienced relatively short drawdowns and V-shaped recoveries – probably because low inflation allowed the Fed the ability to quickly stimulate by slashing interest rates. But quick recoveries are not always the experience. Bear markets are painful because drawdowns are a function of price and time. Since WWII there were 7 bear markets that lasted longer than 9 months (current is 10 months); in those the S&P and NASDAQ indexes declined an average of -30% and -50%, respectively. On average, “long” bear markets last 23 months. Declines were more severe when policy mistakes occurred (1930s & 1970s). The challenge is dealing with both price (decline) and time (duration) as neither can be known. Investors are experiencing a challenging environment this year. At the moment, it appears further time may be required before a new bull market will begin. Time always wears on psyche. The Fed is key; it is being closely monitored as it continues to raise interest rates to rein in inflation. No doubt the financial markets will attempt to surge higher several times off a low and be viewed as a rally or start of a new bull market. But while the Fed is tightening and there exists an inverted yield curve (short term interest rates higher than long rates) – signaling policy mistake(s) and/or recession possibility – this macro backdrop matters. These trends probably need repair before a sustained rally turns into a new bull market. No one knows that date/time; but it will occur. DON’T get emotional and desire to “cash out.” That is a certain recipe for terrible long-term portfolio growth and returns. Doing so always results in lost recovery opportunity. Time is every investor’s greatest ally. DON’T give time away by believing you can successfully get out and back in!

Inversion

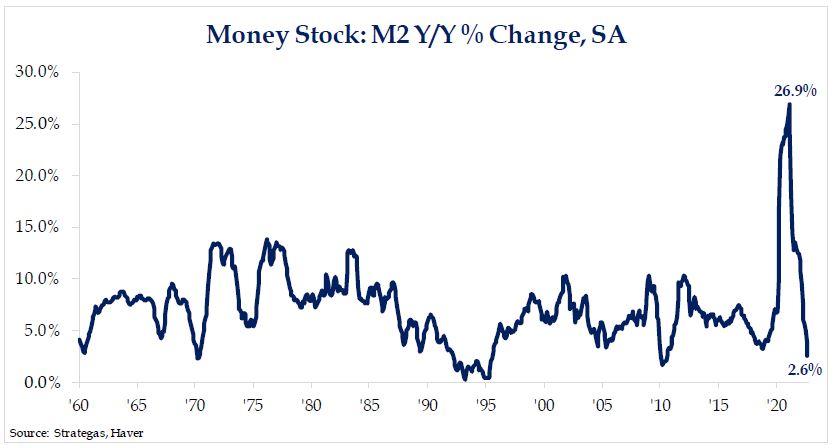

The 14 year experiment with easy (zero interest rates) monetary policy that produced attractive market and portfolio gains is likely over. Inflation resulted and changed it all. In the years following the Great Financial Crisis (’07-‘09), inflation occurred boosting asset values as the global economy grew. Unconventional easy monetary policy is ending and the bill is coming due. In other words, the Liquidity Cycle is likely over. It appears politicians can no longer pursue “bread & taxes” fiscal policies that allow them to spend without any concept of constraint. New, tighter monetary policy may remain longer than many expect as the Fed battles high inflation that is stickier than anticipated. Tight monetary policy includes aggressively raising interest rates plus Quantitative Tightening (allowing accumulated bond purchases under Quantitative Easing to runoff/mature); both reduce money supply (M2) now growing at a 2-3% pace and dramatically down from the nearly +30% rate provided in response to COVID lockdowns. Money supply is used to finance economic growth; normally M2 grows about +5%/year to finance roughly the same pace of economic GDP growth. Money supply growth of +30% when the economy was in lockdown was “rocket fuel” to financial assets as it was not used to finance economic activity. The opposite (inversion) exists today wherein M2 growth is inadequate to support economic growth; likely causing the economy to contract as inflation is being fought. [Financial markets lead the economy and already contracted.]

Money supply is used to finance economic growth; normally M2 grows about +5%/year to finance roughly the same pace of economic GDP growth. Money supply growth of +30% when the economy was in lockdown was “rocket fuel” to financial assets as it was not used to finance economic activity. The opposite (inversion) exists today wherein M2 growth is inadequate to support economic growth; likely causing the economy to contract as inflation is being fought. [Financial markets lead the economy and already contracted.]

The change in Fed policy and money supply growth during 2022 is the first example of inversion; monetary policy is now restrictive. Other inversion themes include: inflation higher for longer; a continued economic growth slowdown; and de-globalization (see Cold War 2.0, below) which is likely at the root of future economic growth and inflation. These changes are showing up in current market action – volatility is higher because uncertainty is elevated. It will take time to sort out what these inversions mean for the economy and future investment winners vs. weaker performers.

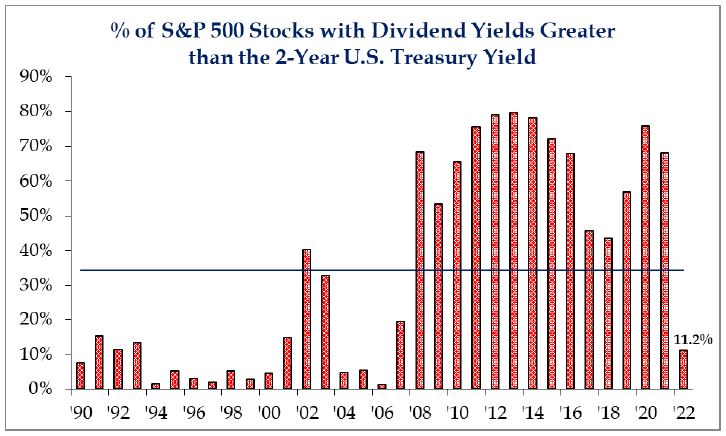

Currently, market action is churning and bifurcated. Energy, industrials, financials and more defensive market areas are leading recent rallies in this bear market. Yesterday’s winners – Tech & FAANG – are struggling with downtrends; they don’t rally consistently as a leader would. The days of cheap financing of “risky” growth is over; investors are requiring financial strength and predictable growth prospects and then valuing the entity using today’s high interest rates. Thus, strong companies that can finance their own growth and pay dividends are performing better. Risk remains at the top – those former “risky” growth leaders who still represent disproportionate share of indexes like the SP500 are vulnerable. Additionally, unlike the last 13 years where 80% of stocks paid dividend yields higher than Treasuries, only 11% do today (another inversion: bonds offer yield again). Key thought – inversions are about change. There is no new liquidity cycle coming to finance risky growth. Don’t get seduced by broken leaders bouncing. Focus on keeping the main thing (bond yields are still rising and monetary conditions tightening), the main thing – follow the leaders (trends); don’t fight the old leaders in downtrends.

Additionally, unlike the last 13 years where 80% of stocks paid dividend yields higher than Treasuries, only 11% do today (another inversion: bonds offer yield again). Key thought – inversions are about change. There is no new liquidity cycle coming to finance risky growth. Don’t get seduced by broken leaders bouncing. Focus on keeping the main thing (bond yields are still rising and monetary conditions tightening), the main thing – follow the leaders (trends); don’t fight the old leaders in downtrends.

Cold War 2.0

Often we receive investment research that is very thought provoking. Strategas, a research firm we highly respect, recently expanded on a theme they introduced a year ago: is China a national security risk which poses supply chain vulnerabilities? Is the US, with others, in Cold War 2.0?

The first Cold War began on 3/12/1947 and ended 12/26/1991. It was a geopolitical, ideological and economic struggle between two world superpowers, the USA and USSR. Starting at the end of WWII, it lasted until dissolution of the Soviet Union. When the Berlin Wall fell in 1989, globalization and free trade was embraced and contributed to low and stable prices for goods and services because of competition (lower wages abroad and cheaper sources of raw materials/food sources). In 2018, national security risks in some industries began to receive some precedent to cheap trade. Then COVID changed everything; supply chains were broken, and vulnerability was exposed that caused many companies to re-evaluate and address challenges. De-globalization is the opposite and underway; it means fewer products for sale, less economic efficiency, and greater political risk. De-globalization places national security as a priority over economic efficiency.

Another byproduct of globalization and the free-flow of capital was lower interest rates and inflation. These helped P/E ratios (valuation) of stocks to rise from an average 13x in 1989 to 19x earnings. It appears this trend is reversing. Biden expanded on Trump’s policies as China and Russia, North Korea, and Iran are challenging the western world order. As these countries are classified as threats, a new official US government policy viewpoint exists and is unlikely to be reversed by a president in 2025. Geopolitical events we are seeing today are likely to become more common.(2) The result is a multipolar world framework where inflation is higher (say 3% instead of 2%); interest rates are higher; economic growth will likely be slower; and valuations (P/E ratios) for investment assets (stocks, bonds, real estate) are lower because profit margins are weaker. It is likely the US and NATO allies will spend more on global defense. Fossil fuels will likely remain a “prize” as noble environmental policies will increase global tensions rather than allay them.

Today, de-globalization is underway; it’s an inversion from the past 44 years. It’s comparable to the first stone being thrown into the pond whose ripples may be felt for a long-time to come; or a spark that causes a forest fire. It’s as Larry Summers calls it, a “hinge moment” in history. The pandemic irreparably damaged China’s “brand” and the ability of developed economies to import disinflation (lower prices). Expect changes in market leadership as the influences of de-globalization and geopolitics play forward. As a result, is value style (with a dividends and cash flow focus) a beneficiary over growth? Is China really investable? China probably never shared intentions of becoming Western apart from its interest in money. [“China gave us the virus. And the free world gave us the vaccines.”] The end of globalization offers implications for inflation, interest rates, economic growth and investing. The challenge – keep investing with an eye on changes occurring everywhere. If one waits to “see” or understand the changing landscape, the market is already moved forward. Don’t lose sight of where you are trying to go, your goals. Stress and turmoil are the bumps on which the market climbs!

(1) Historically, (84% of the roughly 16,000 trading days since 1960), when the Fed was effective in dealing with inflation, their final (terminal) interest rate was higher than inflation (CPI). If the CPI falls back to 3% or 4% in 2023 and the 10-year bond yield is 4% to 5% (higher and above) would be in keeping with history. The terminal Fed Funds rate is always higher than CPI at the end of prior tightening cycles. The Fed will not be happy until inflation drops to goal.

(2) The history of warfare is always there. The NY Times reported the world was at peace for only 268 years out of the past 3,400 years. That’s only 8% of our history that was peaceful. “Wars and rumors of wars” is historically long and will continue for all ages.

Source of most charts including “Peak Inflation” evidence above: Strategas Research Partners

Printer-Friendly PDF Version, including Style and Investment Objective returns for the month.

November 2, 2022