If we owned a crystal ball, we might know when to sell before big market moves down. If we owned a crystal ball, we might also know when to buy at the market low, before big moves up. Would you like to use a crystal ball for your investment timing tool? We know that if you rely on the crystal ball for investing, sooner or later you will be dining on crushed glass. No one owns a crystal ball that works. Don’t attempt to use one.

Given the volatility in the global and domestic markets this past week, it may be helpful to summarize a few thoughts for consideration:

- Past events with flu and other pandemics, like the current coronavirus, will prove temporary. They may create potential for short-term economic impact. Investors often over-react to negative worrisome news in the short term. The Chinese government took some outsized precautions, and others are starting to pursue actions to curb the spread of the virus. These actions will likely slow economic conditions in the first part of 2020 – supply chain impacts probably will slow short-term business and economic growth.

- Weaker global growth does not usually lead to recessions, particularly in the US. America led global recessions in 1975, 1982, 1991, and 2009. The US consumer is currently the strong spot against a global recession. The recent pull-back in the markets because of concern for a spreading virus, may slow near-term consumer spending, but is unlikely to sink the US economy into a recession. US housing is strong and rising because interest rates are low, making homeownership affordable.

- Government stimulus is probably in the ready – both government spending and maybe additional Fed interest rate cuts (though the Fed wants to appear policy inactive in a presidential election year) could be instituted should the economic outlook show too much evidence of deterioration.

- Important, China is pumping money into their economy. Increased money supply, when not used by the economy to finance its growth, ultimately boosts financial asset prices. [Remember what drove US stocks higher in 2019 – excess growth in M2 (money supply) exceeding 10% when the economy was growing at 2%; excess money supply popped financial markets prices higher (maybe too high too fast, as valuations looked stretched).] The response of some policymakers to ease fiscal and monetary policy outside the US is possibly setting the financial markets up for a “slingshot” move in the markets as/when the coronavirus passes.

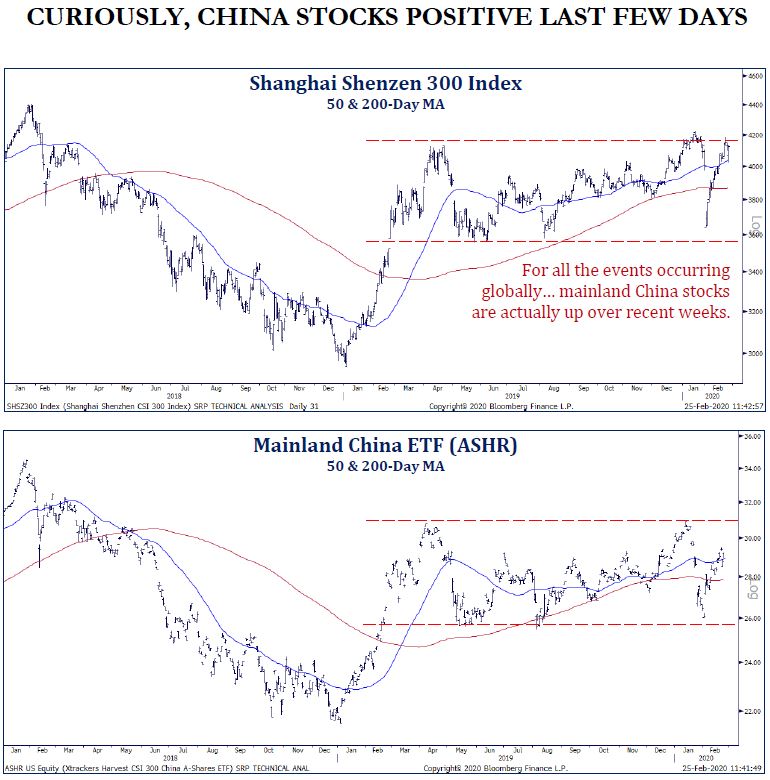

- Interesting to note that the Chinese stock market is already rising. Stocks lead the economy and other events; and China is at the epicenter of this virus worry, yet stock charts show rising trends. Even European stocks (with greater trade activity with China) are showing improving charts (albeit the past couple of days slowed the upward path). Even Japan’s stock market reached a technical low with only 9% of stocks trading above a 50-day average (readings this low are usually attractive buying opportunities for appreciation).

- Tradable lows (in stock prices) need price extremes and investor sentiment extremes. Price extremes are appearing with the S&P500 sliding almost 8% from the February 19 highs. 64% of stocks are trading at 20-day low prices (between 50% and 60% is viewed as a “buy zone” by market technicians). In December 2018, this signal reached almost 95%, and stocks in 2020 advanced nicely.

- US 10-year Treasury yields reached an all-time low yesterday as some worried investors sold stocks and purchased bonds as a safe haven. If bonds were expensive before, they are even more so now (low yields mean high prices). Viewing it differently; 63% of S&P500 stocks offer a dividend yield higher than the 10-year Treasury bond (the historical average is 17% of stocks provide a higher yield). Stock P/E’s declined over the past week from almost 20x to about 17x now. Price adjustments were quick, and offer better value today compared to a week ago.

The news headlines are creating a “peak virus” feel to them. Recall, when most are getting bewildered, or scared, and no one wants to stay at “roach motel”, the markets are close to putting in a low. Investing is often about acting the opposite of your normal intuitions – when things look bad, that is probably a time to consider taking buying action. We are not in the clear just yet. Price action is close, but investor sentiment (worry) is less conclusive; probably requires additional time to wash away recent stretched prices and sentiment, particularly with a small number of overvalued stocks (ie: FAANG stocks).

Please keep your seat belts fastened. Near term market volatility will likely remain elevated, particularly as we move through the spring season of a presidential election year (before conventions). Consider viewing market drawdowns as a “pause that refreshes,” providing an opportunity to invest in the markets at reduced values. Economic growth may slow in the near term, but will likely bounce back due to policy stimulus as 2020 progresses. And these recent events, we believe, allow the current Bull market additional time to run (albeit that it is the oldest running in US history).

Bill Henderly, CFA | Nvest Wealth Strategies, February 26, 2020

Chart Source: Strategas Research Partners