With the midpoint of 2023 now crossed, we hope that your summer is off to a nice start. For the financial markets, things certainly appear better behaved compared with a year ago. In fact, the rebound over the last 9 months is now being labeled by financial media a “new bull market”… yet narrow enthusiasm from just a few stocks casts doubt on that idea. Below are links to access our just published Nvest Nsights newsletter articles, and your personal investment reports will be arriving soon.

- “Lift-off! Do we have Lift Off?” – provides a quick recap about how the 10 largest US stocks is influencing the appearance of broad index performance.

- “Quandary in the Quarry” – Economic indicators continue to signal slowdown is on the horizon? Can the current stock market advance continue and participation broaden?

- “Driving Hands-Free” – AI, or Artificial Intelligence, garnered big hype in the 2Q; the idea of automation everything inspires long-term hope for new gains in productivity, but also creates anxiety. Another form of AI, hands-free driving, can also be likened to how many approach investing… but is it safe?

- “Personal Finance Corner” – An update on how ebbing inflation is beginning to impact savers via iBond rates and what to expect if continued improvement occurs. Also, we briefly review how large or lumpy withdraws can be accompanied by unwanted surprises from Uncle Sam.

Click here for a Printer Friendly PDF which also includes benchmarking and investment data.

Lift-off! Do We Have Lift-off?

Stocks continued to advance in 2Q, even with many confusing negative news stories. Since October 12 (2022; just 9 months ago) the S&P500 advanced almost +26%. This year alone, the S&P500 advanced nearly +17% and the NASDAQ +39% thru the end of June. Many, including the financial media, are now labeling the move as a new bull market because a +20% advance from the bear market low occurred. Lift-off!!! Do we have “lift-off”?

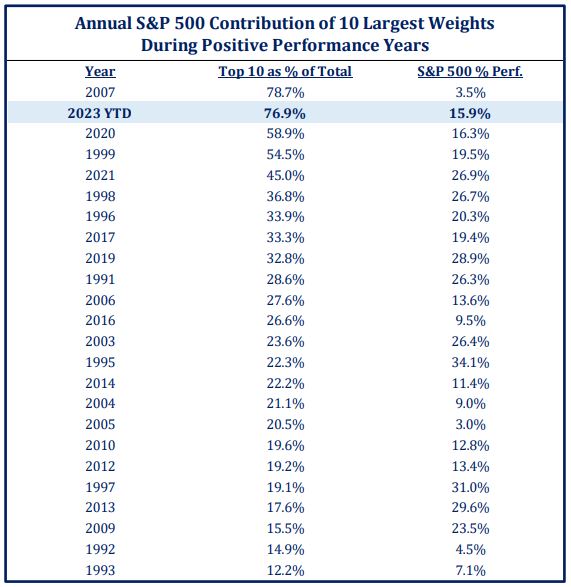

It’s challenging to be convinced that a new bull market is underway when market leadership is so narrow with just 5 mega-cap technology names (making up 24% of the S&P500 index weight) produced over 70% of the YTD advance (largest 10 weights produced 77% of YTD gains). Without their outsized performances and heavy weight in index composition, market gains would be very small. Or, looking at returns differently, non-dividend paying stocks (100) in the S&P500 advanced +18% YTD while dividend paying stocks (400 names) were up only +4%; their worst first half performance since 2009. [Review “Benchmarking” and “Fund Performance” pages to observe performance divergences.]

When the market advances on very narrow leadership or when advances are not broad based, AND when there are a number of market headwinds (monetary policy to battle inflation, with slow money supply growth), it seems unlikely that this encouraging rally over the last 9 months is the start of a new bull market. It’s unlikely we have “escape velocity” to continue a long-term new bull market. Nevertheless, remaining invested is paramount to long-term investment success. If not invested during the past 9 months, the “lift-off” does not occur in your investment portfolio.

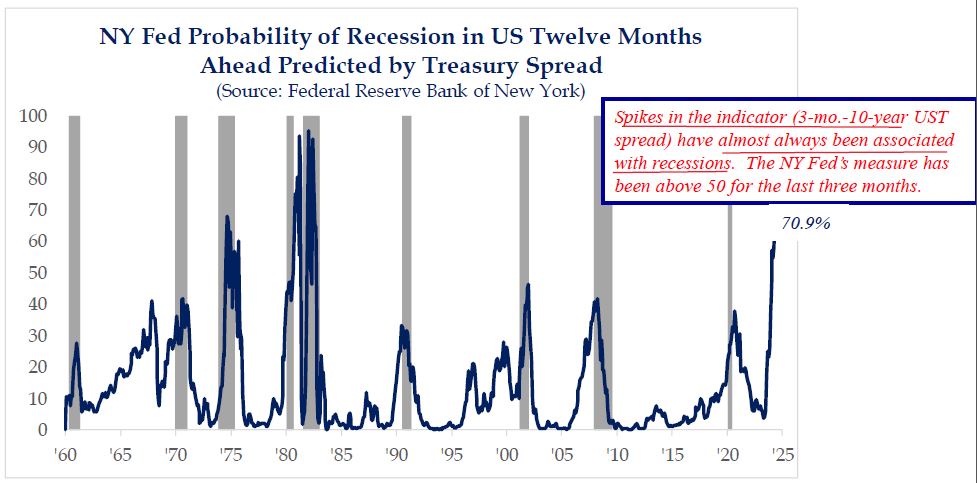

QUANDRY IN THE QUARRY

Are you perplexed? Investors are in a quandary balancing weak economic data against stock market action of the S&P500 or NASDAQ which appears to be looking forward (through) nearly every negative event. While the Fed is raising interest rates to slow the economy and employment to curb consumer demand and inflation, it’s seems difficult to be excited about near-term market prospects for narrow market action. Further, when general news appears so caustic and negative, it’s challenging to get excited period. Let me assure you, this commentary is NOT written to be super-negative, or proclaim as Chicken Little, “The sky is falling.”

The key question to consider – will economic expansion limp along in 2H2023 and into 2024 when there is another presidential election? Can the YTD stock market advance continue and broaden its participation beyond the very narrow?

Let’s review two historical market perspectives, and keep them in mind in the short-term:

- A bear market low never occurred before a recession began. The current (recent) bear market low was 10/12/2022, with the stock market rallying since (see “Lift Off”). Is, or was 10/12/2022 the low without a recession?

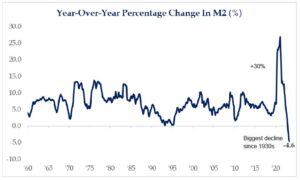

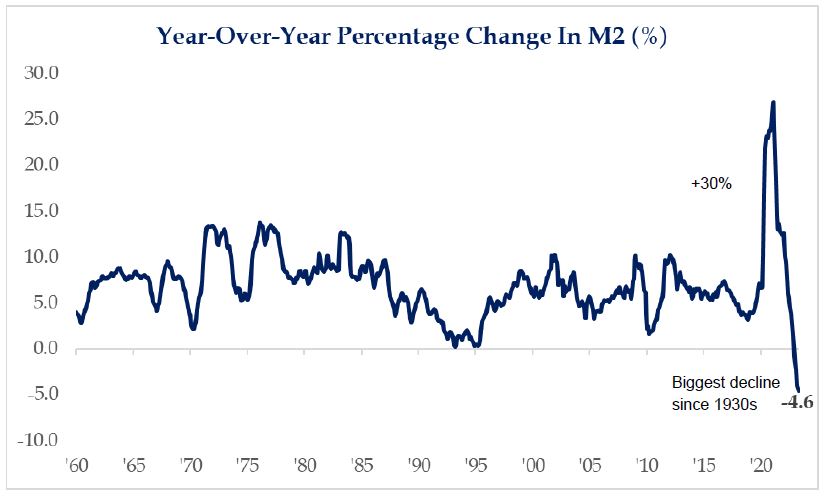

- Is a recession likely? Odds suggest that with the significant decline in money supply (M2) growth (from +30% during 2020-21 to

over -5% now; biggest decline since 1930s); plus an inverted yield curve (where short interest rates are higher than long) for over 12 months; plus a likely continuation of Fed tightening (raising interest rates to battle sticky inflation); with stricter bank lending standards on loans; while the Treasury is issuing large amounts of new debt (post raising the US Debt Ceiling), together are likely to slow the prospect for economic growth and result in at least a mild recession.

over -5% now; biggest decline since 1930s); plus an inverted yield curve (where short interest rates are higher than long) for over 12 months; plus a likely continuation of Fed tightening (raising interest rates to battle sticky inflation); with stricter bank lending standards on loans; while the Treasury is issuing large amounts of new debt (post raising the US Debt Ceiling), together are likely to slow the prospect for economic growth and result in at least a mild recession.

Nevertheless, it’s challenging to argue against the “tape” (market). If an investor was paranoid, anxious, and/or desired to sit on the sidelines to determine when to get in (the in/out decision), investment performance experience is poor.

We suspect market action in the 2nd half of 2023 could be slow until/unless conditions (macro-economic backdrop) improve and broader market participation occurs. Simply, as our June commentary shared, the YTD market performance is encouraging, but may be an Optical Illusion. Keep in mind, bear markets remove excess market risk and usually reveal new market leaders for the next durable bull market advance.

When you are in a quandary about what to do, it’s important to continue to mine for gems in the quarry. Managing investment portfolios should always involve an awareness of risk. Risk is first controlled by the asset mix – stock/bond allocation. That’s called the “investment objective” wherein the long-term stock/bond mix is specified. Once determined, portfolio exposures are tactically adjusted for risk – what areas of the market are attractively valued vs. expensive. Currently, the higher interest rate backdrop that is expected to slow economic growth, promotes owning quality companies with current cash returns (dividends & interest). Our allocation to momentum (growth) strategies currently receive smaller exposures because they are expensive and deemed more risky; they are not excluded (even as they are former year and YTD winners). The portfolio risk management process is ongoing and always key to portfolio performance.

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

DRIVING HANDS-FREE

Do you ever drive hands-free? If so, you probably remove both hands from the steering wheel for only a moment or two, but not long. More auto manufacturers are adding hands-free or autopilot features – a suite of advanced driver assistance systems that can perform a variety of self-driving functions including lane keeping, “safe” car spacing, self-parking, and navigation on roads with minimal or no driver input. Generally, most self-driving vehicles require some operator interaction via steering wheel pressure to operate; they are not fully autonomous systems.

In recent months AI, or artificial intelligence stocks, are taking over as the new investment craze. It appears as the next-gen technology capable of automating “everything” by “computerizing” human decision making via use of mathematical algorithms and existing big data. AI and a few tech stocks are ground-zero of this YTD narrow market performance; the “soup de jour” sector to own. In general, this technology path could represent the ultimate “hands-free driving.”

The idea of “self-driving” or “autopilot” could also be applied to investing. Auto-investing with no fundamental analysis of companies or investment discipline is possible via indexing. Indexing was also well rewarded over the last decade. With hindsight, it seems clear that easy and unlimited access to virtually free money lifted all boats (stocks). Both the well maintained (companies with strong balance sheets, low debt) and those of more questionable seaworthiness (high debt, no profits, etc.) advanced. High inflation and rapidly rising interest rates added “weight” in 2022. Yet it seems a few high-flyer stocks of last year are back in vogue in 2023, even as high interest rate weights persist. We find ourselves perplexed by YTD narrow market leadership because the current macro environment backdrop seems unlikely to reverse anytime soon.

Many experienced investors understand a few factors drive markets – “Don’t fight the Fed” and “Don’t fight the trend/tape” (market) are two key drivers. These are not exclusive, but are interconnected and simultaneous in their influence. Presently, the Fed is pursuing a restrictive monetary policy for the foreseeable future which will slow economic growth and inflation…over time and meaning headwinds exist. Second, “don’t fight the tape” even as valuations may be uninspiring and risk-reward ratios are uninspiring in general. Investor sentiment is one of the strongest current market assets. How is it possible for these two key thoughts – the Fed (restrictive) and the “tape” (encouraging) – to appear contradictory to each other? Which should an investor focus on?

Both apply. There are attractive areas, while others are expensive and risky. 5% yields on short money investments are attractive; highest yields in years. These rates will curb the macro economic environment and also reflect current investor apathy for the stock market via its narrowness. More restrictive monetary policy will cause the economy and job market to weaken; corporate profits are likely to contract (a profit recession). It’s possible for profits to contract without an actual economic recession; but history shares there was never an economic recession without a profits recession. It seems probable that an economic recession will materialize, and by extension a profits recession. Some leading economic signals are beginning to show cracks.

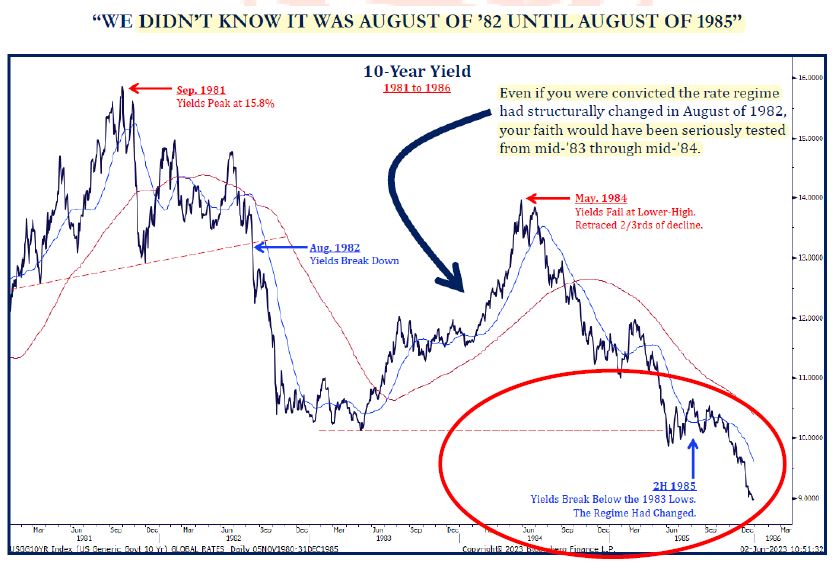

We discourage trying to time the market. That’s because highs & lows in stocks (bonds, or markets) are difficult to call. Great example: when interest rates peaked 42 years ago (1981), several years passed (1985) before investors understood the rules changed. Something as fundamental as interest rates changing in a big way is not immediately understood. As Byron Wien (Wall Street strategist) shared, “Hindsight will offer clarity, while real time speaks with haze.” And, Chris Verone (Strategas technical strategist) added, “there is a casualness of daily changes” that can cloud or hide changing market direction. It can take years before market action fully reveals new leaders; there is a time lag before knowing. While technology and companies poised to be the first beneficiaries of AI are finding investor favor and currently boosting the stock market, we suspect that monetary conditions (high interest rates, low liquidity or slow money supply growth) will redefine the market focus. As this occurs, a shift of leadership toward “quality” is probable. Quality means emphasis on companies with strong balance sheets, proven business models, and a record of paying (and/or increasing) their dividends to shareholders.

Should investors continue to drive hands-free (without paying attention) – blindly owning everything and overweight the most expensive companies via indexing? We don’t recommend it!

-Steve Henderly, CFA | Nvest Wealth Strategies, Inc.

It Takes Time…

Highs and lows are difficult to call. Yields peaked around 16% in September 1981. Then from mid-’83 to ‘84 the world returned to its prior configuration as yields rose sharply. During this time, investors seriously question a regime change before a 30+ year trend of falling rates unfolded.

Could a regime shift be starting today? Tech and speculative growth companies dominated much of the last 10+ years in an era of “free money.” They were hit hard in 2022, but “re-booted” in early ‘23.

Hindsight will offer clarity as to whether yields will remain higher for longer, and a new leadership regime emerges away from expensive tech.