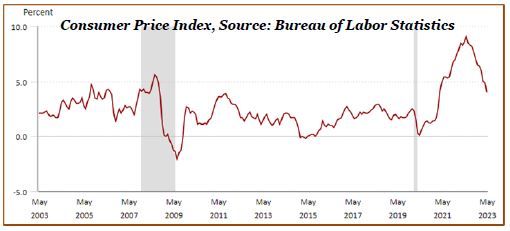

Inflation Begins to Ebb Lower – Impact to Savers

In recent articles titled iPod, iPhone, iPad… now the I Bond and The Upside to Rate Hikes, we highlighted the positive impact of the Fed’s ongoing battle with inflation. Mainly, savers are once again being rewarded with “reasonable” rates. I-Bonds were rewarding savers with rates approaching 10% just a few short months ago!

We continue to receive inquiries about where to “park cash”, including Schwab’s position traded money market funds, which currently yield rates near 5.0%. This rate, as well as other high-yield bank accounts are attractive for those with short-term liquidity needs. However, we caution investors to not become too comfortable with what may feel like the “safe bet”. As the Fed moves towards neutral and rate hikes are paused, saving rates will also likely decline. I-Bond rates are dropping from a peak near 10% to current rates of 4% as the consumer price index (CPI = inflation) declines. Money market rates change daily and are not guaranteed.

Utilizing sound logic to set investment objectives (ie. buckets of time), we encourage clients to stay the course; stay invested. Risk and the corresponding reward go to investors who maintain a long-term view and avoid waiting for the “all clear” signal prior to deploying “dry-powder” pursuant to their long-term investment objectives. History clearly demonstrates that stocks beat bonds, often and by a lot. To stay ahead of every investor’s two biggest enemies, inflation and taxes, one must appropriately allocate between stocks, bonds, and cash. We welcome your questions.

Uncle Sam’s Unwanted Surprises

Many investors know the basics of how money is earned, invested, and taxed in personal and retirement accounts. Recall the benefits of utilizing a qualified retirement plan to defer taxes and build wealth (think 401K, 403B, 457, IRA). These plans are incentivized through tax deferrals, company matching contributions, auto payroll deductions, etc.

Our viewpoint: Tax efficient strategies are prudent for both climbing up the mountain (wealth accumulation phase) as well as descending down (wealth distribution phase).

While building your nest egg through pre-tax and after tax savings is important, there are key tax implications to understand when drawing upon these savings. Large, unplanned withdrawals from any savings or qualified retirement account are often accompanied by unwanted (and future) surprises from Uncle Sam!

Potential unwanted surprises of large, lumpy withdrawals:

- Be aware…Lumpy withdrawals from any invested account during market drawdowns are extra damaging – selling more shares at lower values reduces the ability of the portfolio to recover value when the markets rally.

- Tax on Withdrawals to Pay…more Taxes?!? It’s a “circular” tax experience with consequences.

- Imagine…you made a large withdrawal in 2022. Then in April 2023, additional $$$ are needed to pay taxes on the withdrawal. Then another surprise! You will owe additional income taxes on the withdrawal in 2023 that was for taxes. So frustrating!

- This “circular” tax experience can cause you to remain in an elevated income bracket for several years after the initial large, lumpy withdrawal. Can also occur on large withdraws from after-tax accounts if significant capital gains are triggered.

- Federal & State Income Tax – marginal tax rates increase sharply at various income thresholds; income and taxes are elevated.

- Net Investment Income Tax (NII) – may be impacted by an additional 3.8% tax on investment income for high earners.

- Social Security Income Tax – as income increases, an increasing % of Social Security Income is taxable.

- IRMAA (Income-Related Monthly Adjusted Amount, relating to Medicare coverage)

- Increase to Medicare Part B & Part D premiums

- IRMAA is based on income 2 years prior (i.e. 2023 income will impact IRMAA bracket for 2025)

What to do?

- Build flexibility into your plan

- Save in both pre-tax and after-tax accounts.

- After-tax savings can be accumulate/held in cash at the bank, personal brokerage accounts, & Roth IRA’s.

- Clients with flexibility on where to source withdrawals are best positioned to avoid unwanted surprises.

- Spread out withdrawals across multiple tax years. Planning and spreading out withdrawals across multiple tax years can keep income lower and smoother.

- Financing options – While taking on debt may not be desirable, often working the tax numbers support utilizing certain tools to smooth income (Home Equity Loan, HELOC, Mortgage, etc.)

- Consult your CPA & the Nvest Team prior to making a commitment on funding a large new purchase, to explore the most tax efficient funding method.

As always, our team is here to help study and optimize your cash flow needs. Let us help you efficiently descend the mountain and avoid Uncle Sam’s Unwanted Surprises!