We hope you enjoyed a nice holiday season and are entering 2023 in good health and spirits, optimistic for what the year ahead might bring. For many investors that may feel difficult given the stormy market environment; yet we should each resolve not to give way to unreasonable pessimism either. This quarter we offer several items in our newsletter:

- “Dog Gone ’22!” – some of the most friendly words we could come up with to convey the frustration that most probably feel for the investing experience over the last year, but more importantly a quick review of the factors that influenced both the stock and bond market.

- “Snoozer Cruiser – Dreams for ’23” and “Portfolio Tactics” – We share the key items we are watching; what they might mean for investors in the year ahead; and how we are strategically positioning portfolios.

- “The Upside to Rate Hikes & Secure Act 2.0” – The Fed’s aggressive rate increases last year are not all bad… we share some ideas for how(where) you can get paid significantly more on your cash. Also, some quick highlights about the just passed Secure Act and how it may impact you.

Click here for the Printer-friendly PDF version including benchmarking and fund data

We hope these updates are helpful and encourage you to review. Please do not hesitate to call or email with questions, or to coordinate a time to visit together.

DOG GONE ‘22!

Doggone! Horsefeathers! Fiddlesticks! 2022 confounded most investors’ attitudes and enthusiasm. It’s difficult to regularly save and invest only to experience financial market values evaporating faster than they seem to grow. The title, “Dog Gone” arose from a fleeting view of a street sign in a movie; I thought it was perfect for a commentary title. Recall, “Horsefeathers” was the title of our December market commentary. These adjectives and others – terrible, darn, dang, nasty, rotten, lousy, miserable, vile, scummy, pitiable, and despicable – resonate with feelings about many happenings during 2022. Glad (not sad) that it’s over! “We took the pain, now the gain.” That is often a true life experience; yet the challenge is being unable to know the exact timing for new gains.

The average US stock fund finished 2022 down -17% with the S&P500 losing -18.1%. The 4Q return of +7.6% (strength in October & November) provided some comfort to a “doggone” year. At its worst point last year, the index was off -24.5% on October 12. The stock and bond market struggled with almost all sectors (except energy) experiencing drawdowns. But not all market areas were equally “lousy” or “rotten.” The market tone changed dramatically last year. Past market leaders were “despicable and vile” while new leaders were encouragingly more resilient. The average large value-style stock fund declined -6% while the average large growth stock fund tanked –28%. That relative performance advantage of value over growth is observed in mid- and smaller-size company stocks too. The market tone is changing.

Bonds provided less “miserable” returns than stocks, albeit they too generated negative returns. The core bond fund lost -13% during 2022. Bonds in many cases recorded their biggest/worst losses in history. Together, bond and stock market performance was/is directly tied to the Federal Reserve and other foreign central banks’ monetary policy pivot from QE (easy money policies and zero interest rates) to QT (tight or restrictive monetary policy with aggressive interest rate increases). This monetary policy pivot is aimed at aggressively attacking high inflation – the direct result of big government stimulus and spending before, during and after COVID’s Great Lockdown. This pivot from QE to QT may be one of the most significant changes to monetary policy since 1979. A quote from Mae West seems appropriate, “Too much of a good thing is terrific!” That’s true, until the pendulum swings the other way. 2022 proved the pendulum reached too far a distance from its equilibrium and is reversing. We call that a correction (down less than -20%), or a bear market when stocks decline by -20% or more.

Together, bond and stock market performance was/is directly tied to the Federal Reserve and other foreign central banks’ monetary policy pivot from QE (easy money policies and zero interest rates) to QT (tight or restrictive monetary policy with aggressive interest rate increases). This monetary policy pivot is aimed at aggressively attacking high inflation – the direct result of big government stimulus and spending before, during and after COVID’s Great Lockdown. This pivot from QE to QT may be one of the most significant changes to monetary policy since 1979. A quote from Mae West seems appropriate, “Too much of a good thing is terrific!” That’s true, until the pendulum swings the other way. 2022 proved the pendulum reached too far a distance from its equilibrium and is reversing. We call that a correction (down less than -20%), or a bear market when stocks decline by -20% or more.

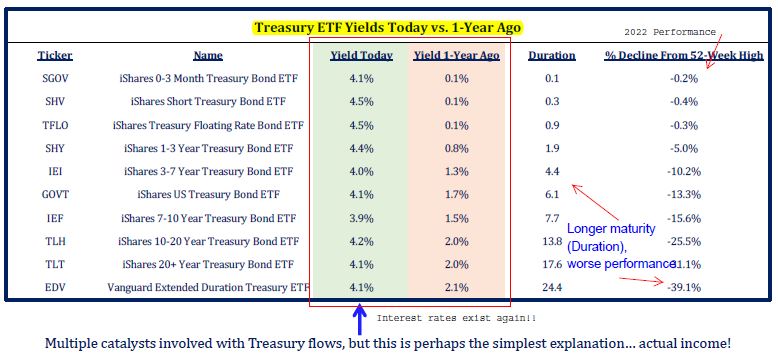

Despite a difficult market experience last year, bonds remain an important portfolio diversifier to stocks. That’s an important point! Recently, bonds did not provide the normal diversification buffer to stock volatility, particularly in 2022 because of QE monetary policies of the last 10+ years. Generally, portfolio diversification that included bonds and stocks, with a focus on higher quality and return of cash (dividends), and exposures to value and unloved sectors like energy buffered client portfolios. Utilizing historically good investment tools – diversification and valuation metrics – in a disciplined process provides long term benefits to growing portfolio values. Today, interest rates exist again; and that means bonds provide meaningful income and diversification benefits again.

What’s the opposite or the antonym of “doggone?” How about wonderful, great, marvelous, commendable, and/or creditable!? As we are at the doorsteps of 2023, we often approach a New Year with optimism and excitement. Yet, following 2022 we very well could be pessimistic and worried. Most important for investing success, now and long term, is keeping time your greatest ally. For investors, that requires remaining invested; not timing the market by getting out and then needing to decide when to reinvest. Do not allow yourself to be unreasonably pessimistic (avoid watching too much news). That is never a recipe for investment success. “Patience is the companion of wisdom” (Saint Augustine).

SNOOZER CRUISER – DREAMS FOR ‘23

Let’s use our imaginations. Let’s dream (anticipate) about 2023. I use this phrase with young kids at bedtime – “enjoy your snoozer cruiser!” Enjoy happy dreams while you sleep in your “snoozer cruiser.” This soft pillowed vehicle can take you places only dreams can travel. No matter our age, we all dream during our sleep. Recall any of your happy, fun dreams? I do; but I won’t recount them here…

Let’s take a “cruise” forward into 2023. If 2022 financial market performance was worse than how the economy performed, it is probable that 2023 may provide the opposite. Might 2023 provide better financial market performance than the economy? Such a timing mismatch is common because the financial markets lead the economy. As the economy is slowing its growth pace due to large interest rate increases (QT), the markets react faster and more severely. Now, as tightening monetary policy is progressing down the path, it is approaching a point where it is likely to be less harsh because the economy is slowing. Financial markets and stocks in particular are looking forward to anticipated changes. On average, the markets move about 6 to 9 months in advance of the economy. That implies that stocks may begin to anticipate a stabilizing and ultimately improving economy as we move through the year. Our “cruise” largely depends on the Fed – how long they keep interest rates high. We expect the Fed to keep interest rates high and monetary policy tight for longer to achieve their goal of beating sticky inflation.

It is widely believed that the risk to economic growth is tilted or skewed to the downside, and is likely to continue to be so for some time as the Fed pursues lower inflation and price stability. Locked into a restrictive monetary policy, we expect that inflation should continue to come down. Additionally, many expect that a mild recession and declines in jobs will occur in 2023 or 2024. Recessions would whack inflationary trends. Keep careful watch – it is government policy mistakes (like fiscal policy – spending, taxes, regulation; and monetary policy – interest rates and money growth) that determine the length and severity of economic slowdowns and market drawdowns; be wary of both occurring together.

History is a helpful guide. First, it teaches there is symmetry to the inflation process – the steeper the rise/increase in price pressures, the steeper the ensuing decline. The declining inflation trend should be the underlying pattern in 2023 and the Fed should ultimately feel less urgency to keep raising interest rates. The key for the financial markets and stocks in particular, is getting beyond the downside risk to US economic growth and company earnings. That’s the forward-looking aspect of the markets.

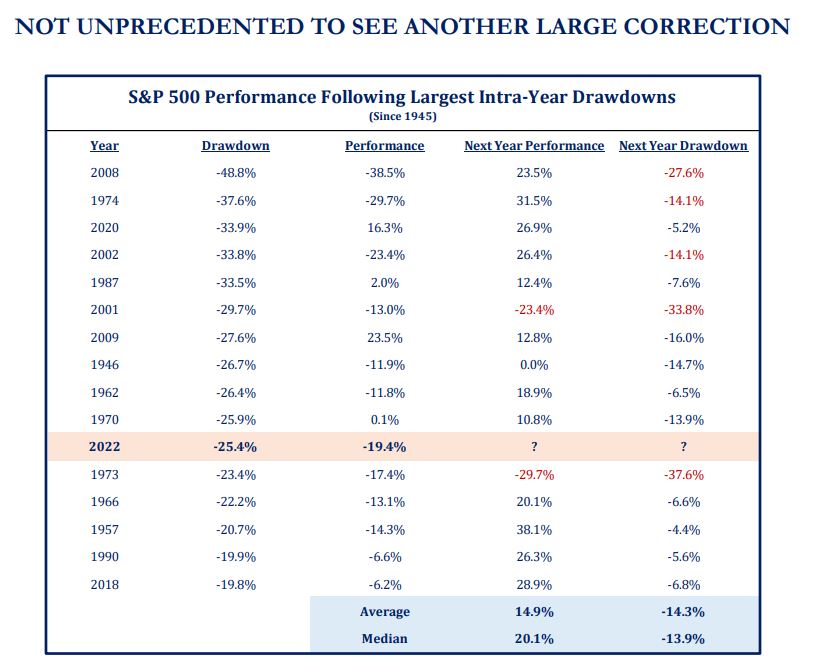

Second, the magnitude of the current bear market (started 1/3/2022) is not extreme, but it is reaching its one-year anniversary. That is rare territory. Historically, bear markets decline about 40% over 20 months. Five bear market since 1950 were longer: 33 months for the 2000 to 2003; 17 months for 2007-2009 (the ensuing 11-year bull market was the longest running in US history), and two others starting in 1973 and 1980 lasted almost 2 years. At the same time however, it is rare to have back-to-back negative stock performance years, and never for bonds. The longer bear markets run, the deeper the correction (the last “bull” market following covid was very short, but does it count??). And that often creates unwanted psychological challenges for investors – it’s the “nightmare” cruise. Thankfully, bull markets historically last about 5 years and rise +180% on average. Remember though, bear markets are a function of price and time, with neither being easy to predict or endure.

Who’s a more successful investor, “Rip Van Winkle” or a “Mental Accounter? Van Winkle was because he took a 20 year nap in his “snoozer cruiser.” He stayed invested, missed much noise/worry, and awoke to exclaim “Wow; look how my portfolio grew!” “Mental Accounter” who watched every market jiggle could not endure volatility; he sold and bought back, but was always late resulting in a poor performance experience. Pace yourself. Be disciplined. Successful investors keep doing the simple – saving, investing, and avoiding the latest investment fads. Ultimately, they sleep and dream better at night.

PORTFOLIO TACTICS FOR 2023

Our biggest 2023 economic themes: 1) higher interest rates for longer because several inflation components will be stubborn, and 2) a shift toward de-globalization seem likely to run for years. This backdrop is creating a leadership shift in the financial markets which we believe will continue. Higher interest rates do not support the previous “everyone gets a participation trophy” orientation (own “junk”, own indexes with everything) that existed under QE monetary policies of the last 10+ years. The pivot to Quantitative Tightening (QT) monetary policies – with higher interest rates for longer – suggest pursuit of a tactical portfolio strategy emphasizing quality and “return of cash.” We incorporated these themes into our tactical strategy over 18 months ago and are encouraged by what we see beneath the “surface” of index performance. Valuation of different styles and areas of the market are always important guidelines in determining tactical strategy. We assess valuation relative to historical averages to understand which areas of the market appear cheap or undervalued and offer better opportunity. Those areas currently include investments with a focus on “return of cash” to investors, and active investment processes. That means pursuing investments focused on fundamentals: dividends, value-style stocks, strong free-cash flow, and less leverage; qualities usually preferred by active strategies (vs. own-everything indexes) because “higher interest rates for longer” changed the investment landscape in 2022. “If the values don’t make sense, then don’t participate.”

Interest rates exist again; there is again a cost of capital (not zero). Portfolios should benefit from higher yields paid on traditional bonds (funds) and thereby support return expectations from stocks. Portfolio returns can be more efficiently derived because returns are not dependent on stocks alone. That also means portfolio construction should/could be less risky and more productive.

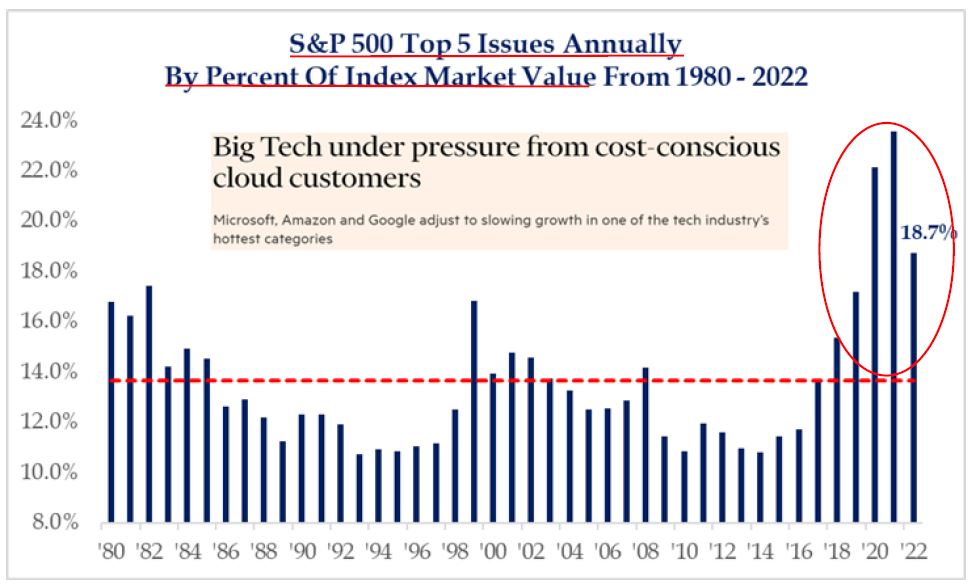

Avoid the “crowded streets” of conjecture; let the market trends do most of the talking. When the “crowd” chases the same ideas, or story stocks, or the investment “soup du’ jour”, or when market charts of leaders appear like a “rocket ship liftoff”, be most wary. When the parade is going down the street with the trumpets blaring and “everyone” wants to own the same thing, be wary; run the other way. Beware of “New Era” thinking (ie: it’s different this time because…). Indexes like the S&P and Nasdaq still appear more vulnerable than the average stock due to a handful of “crowded” ideas (former leaders of FAANG+). In other words, risk is at the top – biggest stock weights in the index. This may create challenge in 2023 for US stocks indexes to outperform compared to foreign and active managed stock funds.

Avoid the “crowded streets” of conjecture; let the market trends do most of the talking. When the “crowd” chases the same ideas, or story stocks, or the investment “soup du’ jour”, or when market charts of leaders appear like a “rocket ship liftoff”, be most wary. When the parade is going down the street with the trumpets blaring and “everyone” wants to own the same thing, be wary; run the other way. Beware of “New Era” thinking (ie: it’s different this time because…). Indexes like the S&P and Nasdaq still appear more vulnerable than the average stock due to a handful of “crowded” ideas (former leaders of FAANG+). In other words, risk is at the top – biggest stock weights in the index. This may create challenge in 2023 for US stocks indexes to outperform compared to foreign and active managed stock funds.

The current market environment is challenging. Yet it offers yields and value that did not exist a year ago. Bear markets refresh exuberant investment approaches that often lack discipline; it allows long term investors to reposition and thereby reap attractive returns.

Author: Bill Henderly, CFA, Nvest Wealth Strategies, Inc. – January 6, 2023

What comes next?

Back to back negative years are a rare occurrence. Often investors receive attractive positive performance after a double-digit losing year such as 2022 (even more rare is 2 consecutive negative years for bonds). That does not mean however that it will be smooth sailing; on average investors a likely to find themselves in a drawdown on the path to a positive full-year result. History suggests a brighter performance is probable, but it will also require “thick skin”.