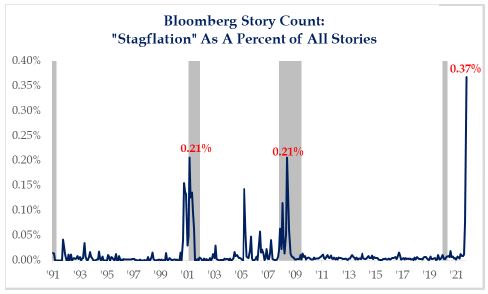

What is Stagflation? Is the US economic environment traveling toward Stagflation? The percentage of news articles mentioning “stagflation” is nearly double (37%) the previous high readings which occurred in the midst of two prior recessions of 2008 and 2001 (both at 21% – see chart at bottom of article). The term stagflation combines two concepts – stagnation and inflation. This condition takes place when economic growth stalls (or stagnates) at the same time inflation is elevated (or rising). Accompanying stagflation is unhealthy levels of unemployment. It occurs when some force or condition increases the cost of production, such as an increase in oil prices (1970s) or a supply-chain disruption (2021) giving rise to the prospects of slowing or stalling economic growth and rising inflation (higher prices). A “supply-side shock” creates shortages of product (could be many products or materials), wherein the price of products rise quickly due to scarcity. Similar to the 1970s, unemployment and availability of workers (today) add to the challenge of slowing economic growth accompanied with rising prices (inflation). If this condition exists too long, it becomes “sticky”, and fighting or managing it becomes challenging.

While this concept is concerning, we may be at peak stagflation talk. That is because we may be at peak, or near peak supply chain bottleneck. When headlines like “The Shortage Economy” (Economist) or “Cargo Crunch” (Barron’s) appear the same weekend, the issue is well known. We may be at peak bottleneck when 72% of companies surveyed report slower product deliveries. Following years of just-in-time inventory management, current conditions will likely require longer to resolve, during which price increases with higher wages create sticky, persistent (not transitory) inflation. During the last 4 months, reported inflation surged above 5%. Longer term, the wildcard is energy. Oil prices are up considerably (87% from a year ago) and create a headwind for consumer spending; rising oil prices are like raising taxes; higher oil prices consume a larger portion of paychecks that might be spent in other places.

While this concept is concerning, we may be at peak stagflation talk. That is because we may be at peak, or near peak supply chain bottleneck. When headlines like “The Shortage Economy” (Economist) or “Cargo Crunch” (Barron’s) appear the same weekend, the issue is well known. We may be at peak bottleneck when 72% of companies surveyed report slower product deliveries. Following years of just-in-time inventory management, current conditions will likely require longer to resolve, during which price increases with higher wages create sticky, persistent (not transitory) inflation. During the last 4 months, reported inflation surged above 5%. Longer term, the wildcard is energy. Oil prices are up considerably (87% from a year ago) and create a headwind for consumer spending; rising oil prices are like raising taxes; higher oil prices consume a larger portion of paychecks that might be spent in other places.

At the same time, economic growth for the third quarter was weak in the US and abroad as demand was restrained by supply. Peak bottleneck should be followed by peak inflation. Clearing bottlenecks is essential. We know that time will cure bottlenecks. It is believed that US economic growth will rebound in coming quarters.

So why did the stock market resume its performance rise in October? Maybe part of the answer is the fact that the stock market is a leading indicator predicting that economic conditions will be better in 6 to 9 months, because supply-chain problems are resolving. Many believe October is historically a bad month for investing; they recall 1929, Black Monday (October 1987), and a couple of other large drawdowns. The 3rd quarter (and September in particular) performance was soft due to worries about stagflation and Washington policy uncertainty. Yet, October generated strong performance with the S&P500 establishing 6 new closing highs and adding +7%. The YTD advance is +24%. The S&P performed well because FAANG, now maybe better labeled GAMMA (Google, Apple, Microsoft, Meta fka Facebook, and Amazon) powered the growth style names higher. Even Tesla hit the “insanity” power boosters. Client portfolios also advanced because large-cap stocks advanced; but small and foreign moved ahead at a slower pace. Recall, foreign is slower at unlocking their economies than US.

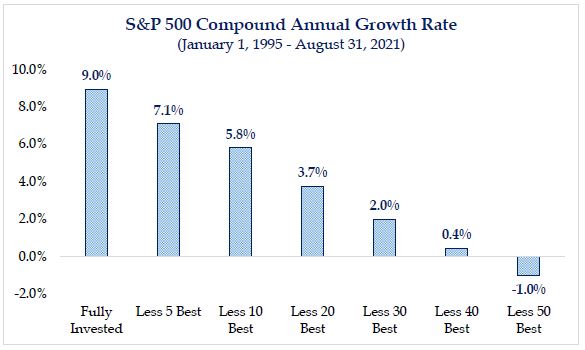

Strong company earnings are powering the stock market higher. In 2020, recall that the stock market jumped higher despite the economy being in the COVID Great Lockdown; company earnings were in a recession. Stocks and all financial assets zoomed higher because of huge government stimulus increases which the economy could not really use (for things like plants, property, equipment, new employees). Valuations of stocks became greatly stretched (prices were up with no accompanying earnings). This year, earnings growth takes the baton from multiple expansion. This is common following recessions – rising stock prices often predict economic growth and recovery, with valuations expanding before earnings growth occurs. Now as fundamentals (sales and earnings) climb, the valuation gap is narrowing. That’s healthy and welcomed. At this point, investors should care more about fundamentals. The path gets trickier as the combination of fundamentals (earnings and revenues) plus multiples (P/E) both drive future returns. Not to get too (more) technical – profit margins (difference between sales revenues less expenses) keep rising and/or improving. That too is a good sign. Stocks tend to not get into too much trouble until profit margins start to rollover or decline. So far 82% of reported 3Q company earnings are beating analysts’ estimates. Typically 66% of companies on average beat analysts’ estimates during any given quarter (back to 1994); this is the 6th quarter in a row for a double digit difference from the average. Meaning: both fundamental and technical market perspectives indicate that this new bull run is still young and on solid footing.

The greatest risk for investors: policy miscues from Washington. Businesses are still not sure on the rules – how will vaccination mandates, taxes, and/or other regulatory proposals affect profitability and confidence? Tax policy proposals can greatly influence future investment returns – tax increases are always a bad pursuit from the market’s perspective. When added to the supply-chain challenges, workers shortage, higher wages, and sticky inflation issues, the “worry” barometer is elevated. That translates into probable market volatility. December could be cueing up for worry (volatility) as the US debt ceiling “can” was kicked down the road from October.

Do you find it challenging to remain focused on long term investment principles? Allow me to share a few comments by legendary investor Bill Miller from his final investment letter of October 20, 2021. Bill Miller is an astute 40-year value-style investor who famously beat the S&P500 for 15 straight years in a row, through to 2005. Miller’s final message is predictably consistent. “Over the past decade or so my letters focused on saying…we are in a bull market that began in March 2009 and continues, accompanied by the typical and inevitable pullbacks and corrections. Its end will come either when stocks get too expensive relative to bonds or when earnings decline, neither of which is the case now.” He goes on to write, “Market timing is foolish – the stock market went up in 70% of postwar years because the US economy grows most of the time. Most of the returns in stocks are concentrated in sharp bursts beginning in periods of great pessimism or fear, as we saw most recently in the 2020 pandemic decline. We believe time, not timing, is key to building wealth in the stock market.” When discussing current worries, from China to inflation, to supply-chain disruptions, he writes, “These are legitimate concerns and seem adequately reflected in the market…One thing I am pretty confident of is that 12 months from now those worries will be replaced by a new set of worries.”

years in a row, through to 2005. Miller’s final message is predictably consistent. “Over the past decade or so my letters focused on saying…we are in a bull market that began in March 2009 and continues, accompanied by the typical and inevitable pullbacks and corrections. Its end will come either when stocks get too expensive relative to bonds or when earnings decline, neither of which is the case now.” He goes on to write, “Market timing is foolish – the stock market went up in 70% of postwar years because the US economy grows most of the time. Most of the returns in stocks are concentrated in sharp bursts beginning in periods of great pessimism or fear, as we saw most recently in the 2020 pandemic decline. We believe time, not timing, is key to building wealth in the stock market.” When discussing current worries, from China to inflation, to supply-chain disruptions, he writes, “These are legitimate concerns and seem adequately reflected in the market…One thing I am pretty confident of is that 12 months from now those worries will be replaced by a new set of worries.”

Bill Miller’s comments are 100% right-on. Worry over current issues is generally unnecessary and not productive; awareness of them is appropriate, but not worry. Worry is the darkroom giant where all your fears get developed. Wise investors pursue time in the market; it’s key to long term investment success. Pursuing a disciplined investment process will lead to success because it is repeatable, over and over again.

Printer-Friendly PDF: Peak Stagflation – Nov2021

Bill Henderly, CFA | Nvest Wealth Strategies, November 4, 2021

There is no shortage recently of media attention on the threat of “stagflation”.