With the 3Q now complete but the stock market seemingly more choppy since September, investors wonder if the final 3 months of the year and 2022 might offer a resumption of upward trend. For most, it’s a difficult consideration amid the confluence of BIG Government-related issues ranging from significant spending and tax proposals (infrastructure and social programs), a potential government shutdown (debt ceiling), whether Fed Chair Powell will be reappointed, and more.

In this quarter’s update, “All of the Above” we review the reasons we see for the stock market losing momentum in recent months, September in particular. We also believe that the Great Lockdown response to COVID will be viewed as a “Pivot Point” in a variety of ways, but including how investors think about inflation, interest rates, and asset allocation. Related, September 30 marked the 40th anniversary of a secular bull market for bonds. What might the next 40 look like?

The personal finance discussion this quarter provides a quick summary of what we see are the most likely tax changes coming as a result of current proposals. As you might imagine, this is a topic arising in most every client conversation this year and we hope you find the quick bullet format helpful.

A printer-friendly version of the full quarterly newsletter, including benchmarking and fund performance data, can be obtained here: Q3 Nvest Nsights

ALL OF THE ABOVE

Multiple Choice: Equities’ performance was choppy during 3Q2021 due to:

A) collateral damage from significant government interventions in the global economy during the last 18 months

B) pieces of the economy are not fitting together well – supply shortages persist, shipping ports are clogged; shipping and energy prices are surging

C) Inflation appears sticky, not transitory

D) the Fed is expected to taper its bond buying program in 4Q (November), but not raise interest rates until later 2022

E) Investors growing concerned about slowing economic growth, or stagflation

F) All of the above.

What’s your answer? Multiple-choice questions that are technical can be daunting when only a basic understanding of the subject exists. They may be easier to answer when the question is very general or when one develops a deeper understanding of topic. Free response answers may be preferred as this format allows sharing understanding during the written response. This economic and market topic area may not be of interest to you, as that’s why you elected to work with Nvest Wealth Strategies in the first place. In any case, the answer was provided via the title of this brief article: “All of the above.”

Investors are continuing to weigh in with their answer via stock market action that reflects a fluid environment during the 3Q2021. The market trend is still upward, but at a much slower pace. Looking below the surface, there is much shifting around; momentum is tepid. In fact, the market index is stuck trading in a narrow range since May 10th. Yet (you say),… the S&P500 managed to establish 21 new highs during the past 3 months, bringing the total new highs for 2021 to 55 with the last being September 2nd. Since then, the market surrendered -5% while the average US stock fund declined -1% for the quarter. That’s the slowest quarterly return since this new bull market began 18 months ago (3/23/2020); it’s only the second negative but worst single month loss this year (January dropping -1%). Many investors are surprised that only a few company stocks were behind the most recent market high; and these stocks are now correcting as interest rates rise. Most investors are also surprised that the average stock declined by double-digits over the summer, and recently over 60% of stocks are trading near 20-day lows. That’s opposite of market action in the early days of a new bull market when the majority of stocks are rising to achieve new highs. It is normal that as bull markets age the number of “soldiers” following the “generals” declines a lot. Rotation occurs with different areas leading and others resting. Important though – the upward trend is still in place. Don’t fight trend even as momentum temporarily wanes.

Another quick question: What stock market sectors are best performing for the YTD?

A) Technology;

B) Energy;

C) Financial/banks;

D) Health care.

If you answered Technology or Health care sectors = wrong. Best guess = Energy, followed by Finance/banks. But during the course of this year, the answer changed a lot with sector rotation.

Client portfolios are a product of the market, as they travel in a similar path with the stocks and bonds. The level of portfolio performance is a function of asset mix – percentage of stocks and bonds. YTD performance returns are attractive; 12 month returns are fantastic, and new bull market returns are unbelievable. The larger the allocation to stocks, the greater the portfolio performances. It is critical to stay invested pursuing an appropriate long term investment objective (stock/bond allocation). Don’t get caught up with politics or other short-term noise; keep watching the underlying economic and business environment.

Question: Is it better to follow emotion when investing? Anyone working with us for a number of years knows our answer: Trying to time the market or “playing it safe” is the biggest risk an investor can take. Successful long term investors remain “time in the market”; we never advocate timing the market (it’s impossible).

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

ALWAYS A PIVOT POINT

A turning or pivot point is when a very significant change occurs; a decisive moment. Sometimes an event in history displays immediate repercussions, making its significance obvious at the time. Other times, the impact of an event or decision, or person is clear only in retrospect. There are always pivot points occurring, but not all create dramatic moments. We believe the US and global economic system is experiencing a pivot point. Time will tell, in retrospect, as to how significant is this point. The pivot was initiated with the Great Lockdown resulting from COVID, wherein governments flooded the financial system with support and aid. Now, in late 2021, we are moving away from maximum policy accommodation and stimulus as central bankers begin tapering off their bond buying activities; they also state that they are not yet ready to begin raising interest rates, a tightening monetary policy action. Government fiscal (tax, spending and regulatory/tariff) policy is attempting to remain in full “spend” mode. The pivotal question: was policy action – that “broke all the rules”, where “every snap was an audible or a broken play” creating huge deficit spending – the catalyst to sticky, stubborn inflation and higher interest rates? Savers welcome higher interest rates (nonexistent for 15 years). Recent and current policy action may, when looking back, be the pivot or turning point.

September was a “month to remember” as the Administration and Congress are confusing the public focus on a bipartisan infrastructure package, plus an additional $3.5 trillion spending budget (all social program oriented) with huge tax increase ideas, a potential government shutdown, the debt ceiling, and the reappointment of current Fed Chairman Powell. That uncertainty appears to not yet be ending and is creating a nervous bull (investor). These political pursuits are occurring on the heels of massive monetary and fiscal stimulus that started in 2020. Amazing, many of the current economic stats indicate our economic recovery at, above and beyond the pre-COVID levels; except for unemployment. At this point, US job openings are going unfilled, with unemployment still 5 million higher than pre-COVID levels. We read reports of the past wherein 100 people might apply for 1 job; today, there are only 10 applicants and many do not show up for their interview. Many employers cannot find qualified workers. That translates into small businesses reducing working hours, even closing; and raising prices to cover increased wages and supply costs.

Could this translate into a challenging former economic condition, called stagflation (experienced during the 1970s)? Could we be pivoting to a stagflation economic environment over the coming years? Stagflation gets its name from stagnating (slowing) economic growth (outlook) with rising inflation. Inflation can become a stubborn, sticky component that is difficult to alter. The Great Lockdown (2020) altered the US and world supply chain – raw materials, manufactured products and components, and shipping (boat, rail, truck) – causing the price for most everything to rise. There does not appear any signs of cost pressure (+9.7% year over year) being alleviated soon. Unable to find workers, and unable to meet increased demand, companies are deciding to produce higher priced products in smaller quantity with the hope to maintain product revenues and profit margins even while paying significantly higher wages. The product supply problem does not show immanent resolution. The longer the supply-chain bottlenecks and employment shortfall exists, the more sticky inflation will remain, creating a greater challenge to control thereafter.

Investing during an environment of sticky, stubborn inflation, or stagflation requires investing in stocks, including those growing their dividends; also owning convertible bonds enhances returns. During inflationary times, bonds do not perform well as their interest payments are fixed; they cannot grow. Bond issuers like inflation, as repaying the bonds is with less valuable dollars; savers dislike inflation because it erodes the value of the cash flows. To beat inflation, Investors need growth assets – stocks, real estate – that can receive price appreciation. We are not advocating owning all stock portfolios. Bonds offer diversification, liquidity, and enhance your flexibility from where to source money in a variety of market environments. Owning bonds requires careful focus on maturity and quality – owning bonds issued by better financed companies, and shorter maturities due in 5 years or less (provides re-pricing opportunities during inflationary times). History shows that stocks are good inflation fighters. Don’t fear pivot points; it is important to keep investing via correct asset choices during that time.

-Bill Henderly, CFA, Nvest Wealth Strategies, Inc.

HAPPY ANNIVERSARY

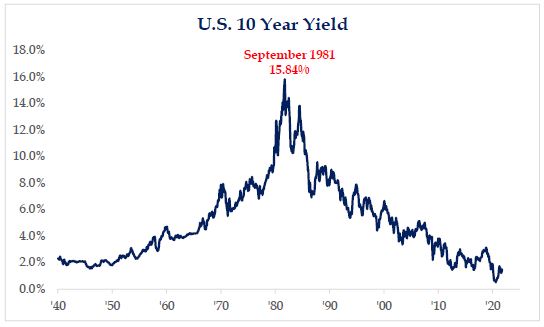

September 30 (quarter end) marked the 40th anniversary of the current bull market for bonds. Happy Anniversary Bond Bulls! This bond bull market started September 30, 1981 with historically high interest rates of 15.84% on a 10-year Treasury bond (mortgage bonds provided yields of 18.75%). Inflation was sky high; it was hyper due to a quadrupling of oil prices in 1974-75. The prime (short borrowing) interest rate was over 20%. I can attest…, no one enjoyed investing during this time. Stocks struggled greatly, and investors were leery of owning bonds at 18%; who would want to borrow money and pay 18% (that’s junk bond rates; that’s credit card rates today)?

Hindsight is 20/20, but foresight is legally blind. Hindsight would advocate buying all the zero-coupon (rate) bonds available – they were priced at a compounding 18% rate which means there is no re-investment rate risk; you earn 18% per year until maturity. 18% compounded for 10 years is better than the average annual 10-year return on stocks. This was a layup which investors did not want because they could not see how the “back of inflation” could be broken. Inflation is not an investors’ friend; it is one of our two investment enemies (other being taxes).

Then in 1981 President Reagan and Congress cut income tax rates (top marginal rate was 70%!) in half. That initiated, or was the pivot or catalyst for a 40 year bull market in bonds. A bull market in bonds occurs because interest rates fall. Recall, as interests rates fall, bond prices rise. For the last 40 years, interest rates were on the glide path of a brick – downward. As you know, the last 15 years, with ZIRP (zero interest rate policies) paid on savings and bonds is next to “zero”. Savers earn trivial interest.

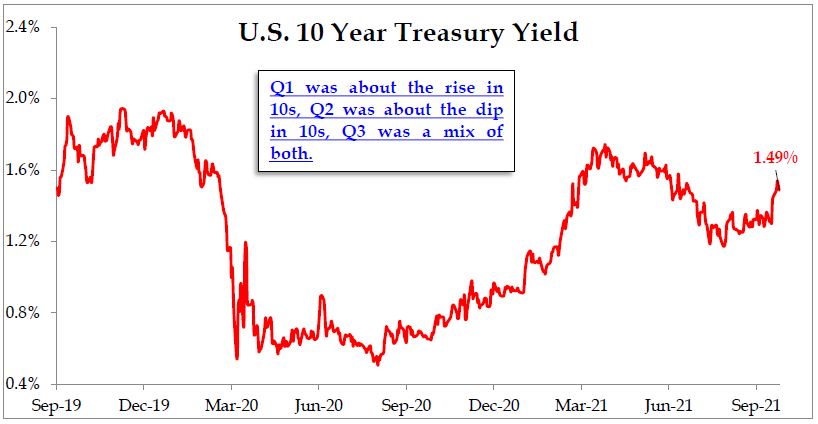

Forty years later, we may be at another inflection point. The 40-year bull market for bonds may be ending, meaning rates may be starting a trip upward. That’s because of current uncertain inflation expectations – is it becoming sticky and stubborn? Even in 2021 we can see three distinct yield phases for the 10-year Treasury…1) January to April: yields went from 0.9% to 1.75% (big move up); 2) April to August: yields fell from 1.75% back to 1.15%; and 3) August to today: yields rising to 1.50%. This is likely because of too much government spending, supply-chain bottlenecks, and rising inflation everywhere while the economy recovers from the Great Lockdown. Even oil and gas (briefly discussed above) is hitting the highest prices in years (creating inflation). Bond investors are trying to anticipate current government policy action, and are concerned about the US government deficit situation and prospect for higher taxes.

Are these “fun” times for savers and investors? If the bond bull market is over, the “fun” appreciation environment for bonds is complete. Investors must pay close attention to bond quality and maturity. All investors must continue to monitor changing US and global government policy actions in the form of spending and taxes; economic growth conditions, and the path of inflation expectations and interest rates. Savers should welcome higher interest rates (to a degree). Don’t be unnerved. Owning stocks is very important to combat the effects of inflation. Historically, dividends contributed nearly 50% of the total return over time based on data going back to the 1930s. Stock dividends are likely to be more important as we pivot throughout the 2020s. It is important for diversification benefits to own both bonds and stocks, even when inflation appears to be sticky.

Did you know?….Nvest Wealth Strategies celebrated its 15th anniversary this year? Nvest was “born” in May 2006. Thank you for asking us to be your investment advisor and assisting you with LIVING LIFE financial planning. Thank you for sharing our services abilities with your family and friends.