It is often said that there are just two certainties in life: Death and Taxes. Or how about “the only constant in life is change”? In 2021, it is hard to recall a client conversation where the topic of potential tax policy changes did not arise. Since COVID, government policy was all about huge stimulus and spending; as we shift our attention to the final quarter of 2021 and beyond, the conversation is increasingly about how all additional spending proposals will be paid for (via taxes – both corporate and personal).

What are we hearing/reading on proposed tax changes being debated; what’s likely to occur? While we do not hold ourselves out as tax professionals (nor intend this as tax advice), negotiations by policymakers are ongoing. Remember, investors have two enemies—taxes and inflation. Below is a quick summary of key tax increase targets:

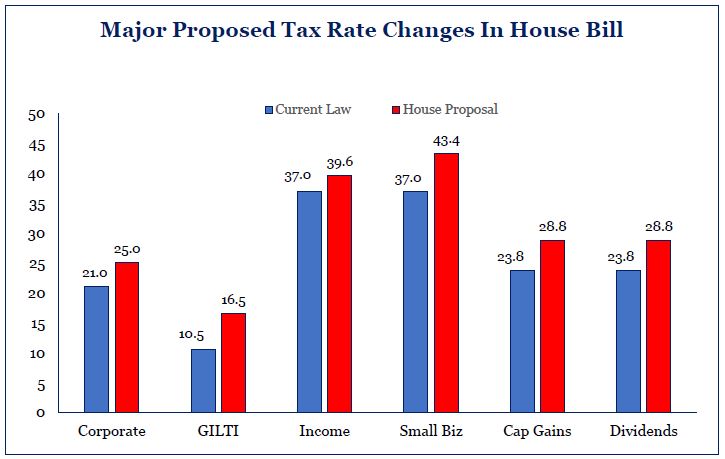

- Income and taxes on capital gains: tax rates are proposed to rise for households making $400k/year or more. Capital gains for those same individuals could rise to an effective rate of 28.8% when also factoring in the 3.8% healthcare-related surtax (vs. 23.8 currently); earners at $1 million+ would see capital gains rates at 43.4% (vs 23.8% currently).

- Corporate Tax rates: may increase from 21% currently toward 25%, reversing much of the 2017 corporate tax cuts.

- Small business owners with >$500k of income will see their taxes increase while losing some meaningful deductions.

- Value of itemized deductions may be limited to 28% – meaning high-earners would receive a smaller tax benefit than heretofore for things like charitable donations, traditional retirement account contributions, mortgage interest, etc.

- Many tax people suspect the $10,000 deduction cap on combined state and local taxes (SALT) will be eliminated; meaning that payment of all state and local income/property taxes could become deductible again; increasing the probability that itemizing deductions is more attractive vs. using the standard deduction;

- Estate taxes: the lifetime exemption may be reduced from current $11.3million/person to $6million/person effective in January (4 years ahead of schedule) – meaning the estate tax would be a wealth reduction factor for more families than current.

- It seems increasingly unlikely that an originally proposed change to eliminate the beneficial step-up basis will survive; this would tax the appreciation on assets (including real estate, small businesses and farms) moving to beneficiaries of an estate.

- Roth IRA Conversions: may become more tightly restricted. Proposed legislation may eliminate conversion of after-tax IRA contributions to Roth (no more “backdoor” Roth contribution) starting in 2022. If income is more than $400k, one could also be prohibited from converting pre-tax retirement money to Roth IRA accounts after 2032.

- “Mega-Backdoor Roth” provisions available in a few (but growing number of) company 401k plans is being considered for elimination (this seems like low-hanging fruit).

Based on respected Washington policy research we receive, those with annual earnings below $400k should worry less about many of the proposed changes. For those above that threshold or with large estates, changes appear significant. These wide ranging, massive income and wealth tax changes would not be received well by the financial markets if fully implemented; they would represent the largest tax increases in over 50 years. Tax increases (like inflation) lower investment returns and wealth. On the other hand, the failure to enact these huge tax changes would be bullish for all. If it’s been a while since we updated your LIVING LIFE projections, or if you are concerned about how some tax proposals may impact your current savings or giving strategies, we invite you to connect with us so we can review your personal plans together; we can help determine if any additional strategies may be appropriate to explore.

Author: Steve Henderly, CFA | Nvest Wealth Strategies, Inc. – October 7, 2021

Source: Strategas Research Partners